The Shift to AI-Native

A New Era of Software, Infrastructure, and Interaction

The Reports of Cloud Software’s Demise Are Greatly Exaggerated

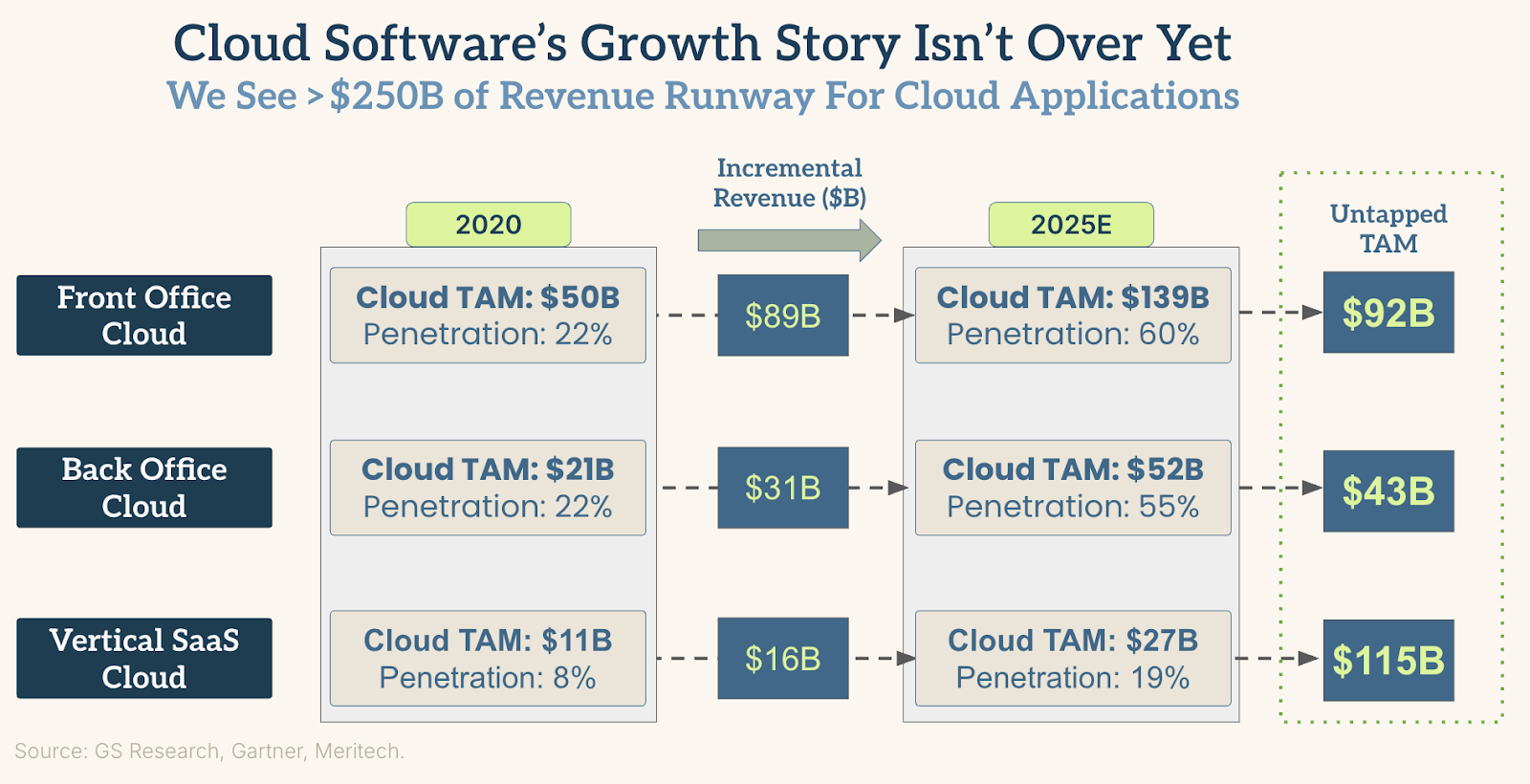

Over the last 11 years, business software spending has grown exponentially with Forrester and Gartner projecting annual worldwide SaaS spend will surpass $1T this year. Here at Bowery Capital, we believe that the chatter in today’s market about the end of B2B software is greatly exaggerated. While the cloud software market has matured immensely over the last decade, it still remains large and growing, and in many sectors digitization is far from complete.

If you look at this chart above - which outlines some of the core business application categories - you can see that aggregate spend more than doubled across each of them between 2020 and 2025 (big thanks to our friends at Meritech for pulling together some of the underlying data for this graphic). And based on today’s penetration rates and digitization trends, we estimate that there remains at least another $250B of software spend to unlock in the coming years across horizontal front-office/back-office and vertical SaaS.

These underlying addressable markets will also continue to expand as software use cases evolve in the coming decade and we continue to see opportunity in software and the cloud. And now, AI is poised to act as a catalyst that will supercharge this growth by making software more useful, more automated, and easier to implement.

AI Is The Ultimate Accelerant

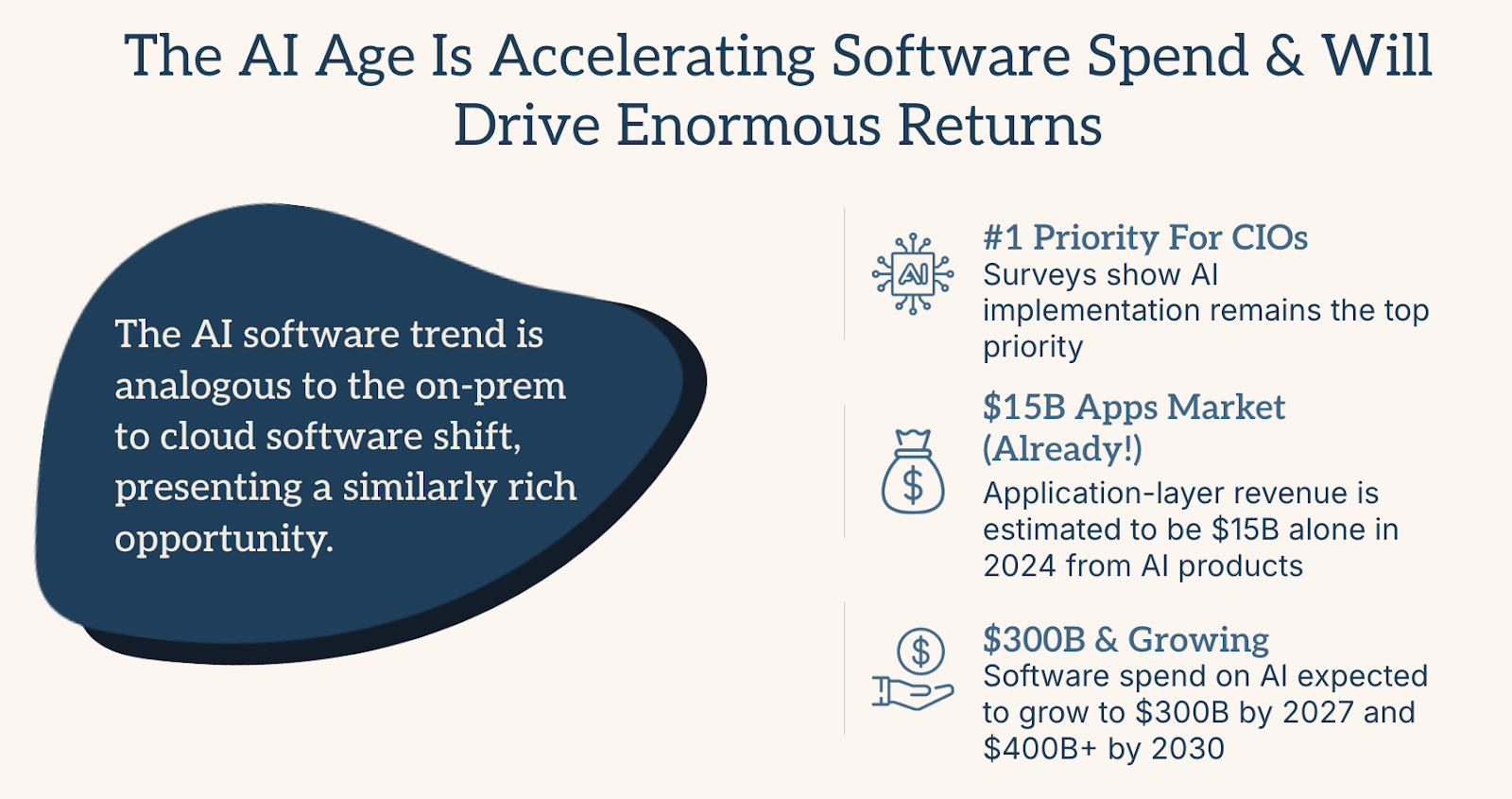

Our collective entry into the AI era is leading enterprises to prepare for the next major platform shift. We think the shake-ups and new opportunities that will arise from the widespread adoption of AI will be analogous to what we saw during the shift from on-prem to the cloud.

Just two years post-GPT, we are already seeing billions of dollars of spend on AI-native apps, incumbent up-sells, and prosumer applications. AI is the top priority for today’s CIOs; and enterprises have been quicker to adopt AI than we saw in the cloud platform shift, as incorporating AI is increasingly seen as a critical business need.

Gartner anticipates that spend on AI apps will surpass $400B annually by 2030 and we see unique opportunities in terms of the available white space and potential land grabs over the next 5 years as the AI cycle takes off. When we think about how AI impacts our role as investors, we see both horizontal and vertical opportunities emerging.

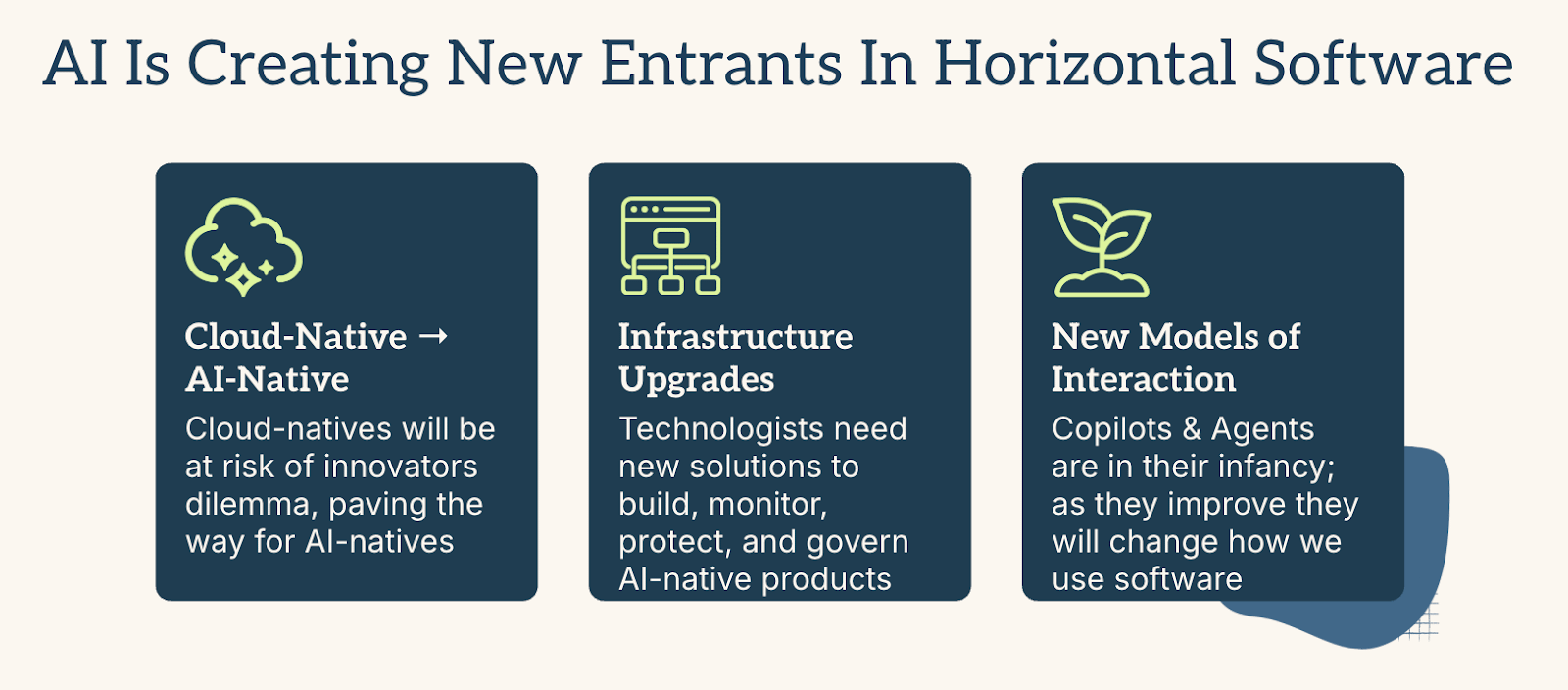

AI Is Creating New Horizontal App & Infra Entrants

In terms of horizontal business applications, we see a huge opportunity around the shift from cloud-native to AI-native. The same way some incumbents struggled to move from on-premises to the cloud, the shift to AI-first products will inevitably see some incumbents do well, while others will flounder. This kind of platform shift is often where you can see very large horizontal challenger applications emerge.

Horizontal infrastructure is an area we are particularly excited about. AI necessitates a new set of infrastructure tooling and new takes on existing solutions around security, observability, and data management.

In terms of new modes of interaction, business-oriented copilots (barring some big, big exceptions like Cursor) have received an underwhelming reception in the market. However, we see much greater promise in AI agents, and as they improve, they will completely reshape how businesses deploy and pay for software.

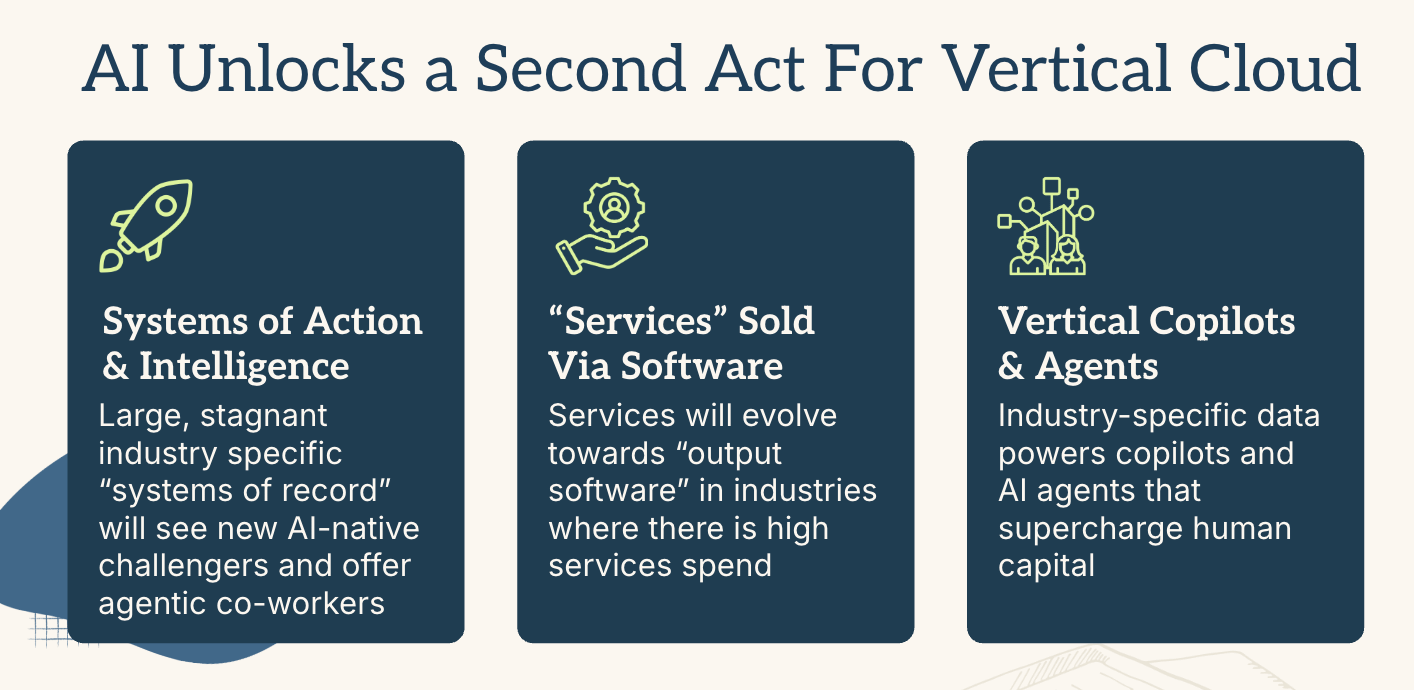

AI Unlocks A Second Act For Vertical Cloud

AI’s capabilities are also creating a second act for vertical software; systems of record are becoming systems of action with the next wave of vertical software being focused on outputs vs. organization. While vertical software has gotten very hot amongst the VC class in the last 18 months, there are some very good reasons investors are flocking to a business model we have been backing for ~10 years.

Vertical AI businesses are growing faster, commanding higher ACVs, and showing better unit economics than existing industry cloud players. Some examples to track here would be Harvey (in law), Hebbia (in finance), and Abridge (in medicine).

We also think vertical apps are more defensible than horizontal startups against the threats posed by the foundation models. While OpenAI might build an AI CRM or AI SDR app if their subscription or API revenue begins to lag, they are probably never going to build an app for water utility management or an enterprise command-and-control center for franchising (these are just two examples of where we have placed vertical bets). Vertical AI, while selling into smaller end-markets and having more winner-take-all dynamics, are actually insulated from direct competition with foundation models in a way broad horizontal apps are not.

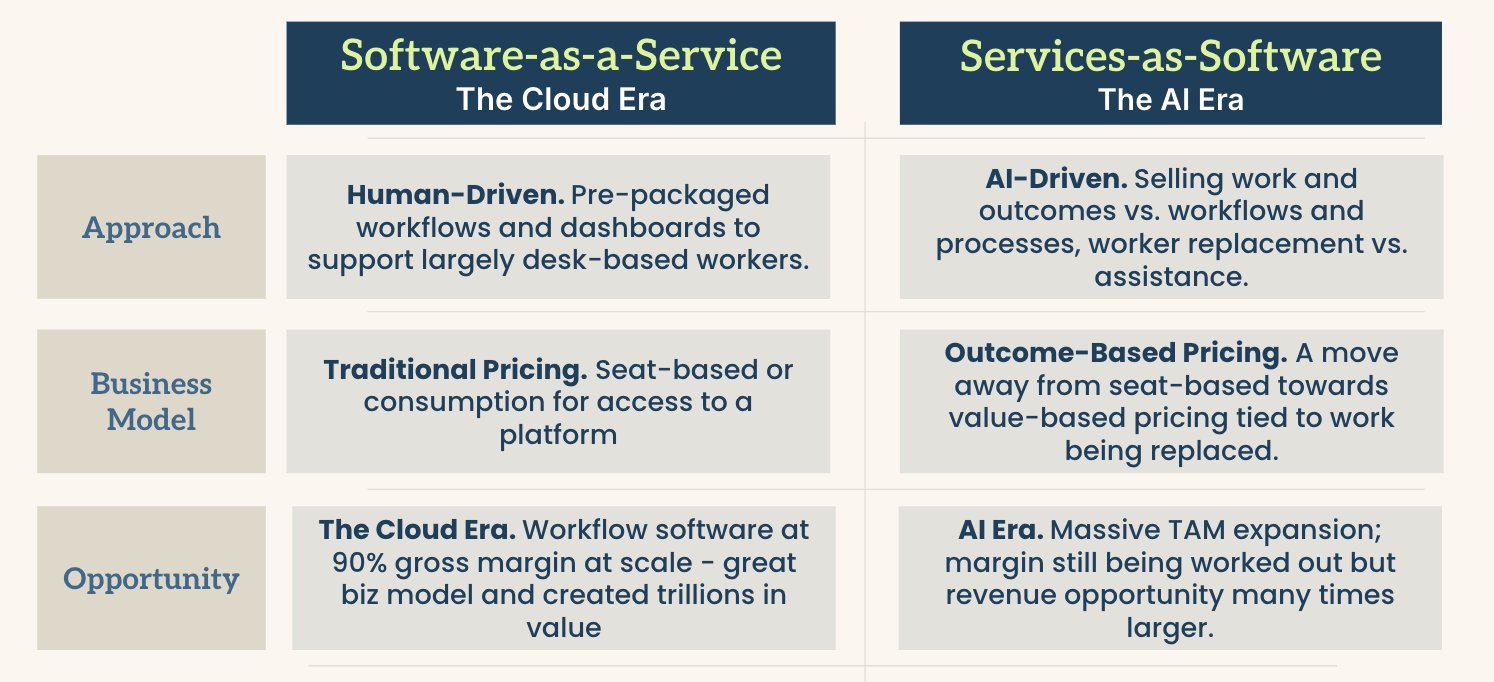

AI Agents Mean Software Can Draw Upon IT And Human Capital Budgets

AI workers have arrived, and software is how they will be provisioned and managed. We are looking to invest behind the potential for agentic AI to enable software to move out of the office of CIO and dip into much larger human capital budgets. This trend is often framed as the shift from Software-as-a-Service to Services-as-Software.

As AI-enabled software evolves to be capable of completing entire jobs vs. just offering an assist, it reframes the discussion around the kind of contract values a startup can command.

One uncertainty here is that while the market opportunity is huge, pricing and delivery of Services as Software is still evolving - however, we think the potential for market and use case expansion more than offsets any lingering uncertainty around monetization structures. And new approaches towards pricing and delivery of software is something we are excited about as AI-native use cases begin to outstrip traditional SaaS frameworks.

Just as Bowery’s first decade was defined by legacy on-prem software being replaced by cloud-native, browser-based apps, the shift towards AI-native apps (and the disruption they will bring) will come to define our next decade of investing.